Is the Insurance Industry about to change radically?

While Insurance is a massive industry, for example net premiums for life and P&C insurance the US are estimated worth around $1,000,000,000,000 (yes that is twelve zeros) I believe it has just been barely affected by the massive software driven changes that other industries are experiencing.

At core, the Insurance industry is impacted by the same underlying trends as the Banking Industry:

Transparency

Online comparators have brought unheard of transparency in pricing. In markets such as the UK, 56% of consumers declared having used a price comparison website in the last 2 years. This is no exception that Google started its move in the insurance space there. In the US, a growing number of companies are looking to play this role, positioning themselves as broker with examples such as Coverhound and Policy Genius.

But that transparency is starting to expand beyond just pricing but how an insurance policy covers an individual’s risk at granular level. In mass market, insurance products, while relevant to the risk profile of the individual from the perspective of the insurer, tend to lack detailed granular level from the perspective of the customer. Companies, such as Trov (disclosure: Anthemis is an investor), are helping to create this customisation in the Home Content insurance by allowing coverage of key items vs having a policy with a coverage set with averaged amounts. Metromile is another example in the motor insurance industry.

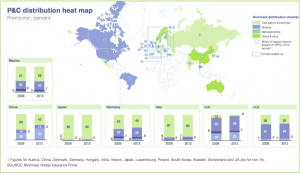

Impact of Digital on Distribution

The Insurance Industry, due to its specificities, has evolved to a reseller model (whether captive or independent). However with online distribution channels becoming increasingly primary channels, will the insurance agent suffer the same fate as the bank branch? As digital distribution channels prefer scale, it can be expected that markets with a large number of small broker players will face intense consolidation going forward, as shown by the rapid consolidation of the UK insurance market. The success of Direct Distribution models in some countries, including China, can also be be a hint to what is coming next. Will the brokers be disintermediated? Or will they find new value add activities to justify their existence?

Source: MCKinsey Global Insurance Industry Insights

As we have seen in other industries, it is very difficult to turn itself into a digital first company. It may sound cliché but the Innovator Dilemma effect is playing at full when most of your current revenue base depends on traditional distribution / management methods. We are just starting to see the emergence of new digital first carriers, with companies like Oscar leading. Oscar’s mobile experience not only reduces its operational cost but helps redefine the link between carrier, customer and physician and potentially affect risk levels. It also provides a flexible platform that can adapt to emerging new technologies such as wearables.

Oscar’s partnership with Misfit

From a Venture Capital perspective it is an expensive proposition with an important part of capital required for regulatory requirement but taking a longer term view, these balance sheet companies may turn more attractive in a regularised rate environment.

Beyond, if you think of insurance as a class of exotic financial products, is there a possibility for larger scale disintermediation similar to banks and alternative lending possible for carriers and alternative insurance funds.

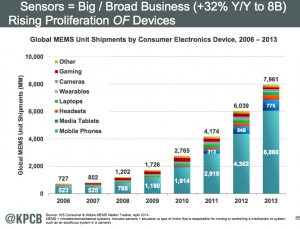

Big Data

Insurance is in many ways the historical big data business and in trendier places, one might be able to call actuaries data scientists. One of the historical asset of insurance is in its past loss data. However with the exponential growth of sensors in our world new sources of data emerge (see Metromile as well)

Source: KPCB

Additionally companies such as Google, Facebook or Amazon are more likely to have attracted top data talents than traditional carriers. A good example is the success of Climate Corporation (a former Anthemis portfolio company, founded by an ex-Google employee and acquired in 2013 by Monsanto. By leveraging publicly available weather data including the large network of weather stations maintained by NOAA in the US and combining it with a modern big data infrastructure built from the ground up, Climate Corporation was able to provide instant weather insurance quotes.

In the B2B insurance world, for the most part, Lloyds of London still relies heavily on email and excel. When databases exist, they are often siloed from each others and sits in technology that makes live manipulation of data very difficult or impossible. Companies such as Quantemplate (disclosure: I am a non executive director and Anthemis is an investor) bring data efficiency to players that have been struggling with it. The ability to manipulate complex data has the potential to reinforce an algorithmic approach on risk in these markets.

However, perhaps even more than banking, I believe the insurance industry will be facing fundamental challenges in the near future. One way to think about it is perhaps to start again from the definition of insurance itself.

Insurance is a form of risk management primarily used to hedge against the risk of a contingent, uncertain loss. (Wikipedia)

Risk

The combination of an increased number of sensors and computational abilities has the ability to largely impact existing pools of risk. The car industry is a typical example. Statistics tend to show that the human factor a.k.a the driver is the first (by a large percentage — 94% in the US) cause of accidents. Looking further into the statistics the first two reasons are recognition error and decision error for a total of 75%. While fully automated cars may be sligthly further away in the picture, machine assisted driving is on the verge of becoming available in the mass market. Whether via radars or sensors, self braking mechanisms are being deployed by car manufacturers.

[embed]https://www.youtube.com/watch?v=omHES8mqtW4[/embed]

To put this in perspective, motor insurance represent about 30% of overall premiums for P&C insurance in Europe. With lower collision risks, premium will be expected to lower as well (and the additional cost of electronics onboard will not compensate for the difference). One of the underlying question is whether with lowered premiums and less variability per driver, the insurance could be embedded in the cost of the vehicle itself. At what point do insurance and guarantee start to look more and more the same?

As software is having more and more impact on our life, the question on risks attached to it, whether digital reputation, or impact of software failure in the real world is becoming more and more important. Will risk shift to software provider away from individuals and traditional companies. For example, should Google or the user be insured for a Google Car?

Contingent

With more and more sensors accompanying us daily and measuring the way we move, eat and feel, is the level of contingency on an individual’s health shifting? There are several experiments by insurance companies in leveraging wearables for prevention in health plans. Oscar is running a specific program with Misfit and Vitality‘s insurance program has a strong focus on prevention. From a strategic point of view it makes sense for insurers to run this type of programs as they might benefit from an indirect self selection process, assuming people wearing wearables are more health conscious than the average population and have less exposure to certain risk (an equivalent of the original Progressive strategy in car insurance).

Alongside sensors the progress in genetic testing (speed and costs as well as the increased ability to run large statistical research) will also ask for a clarification of the role of insurance / and who should provide it (educating myself on this topic so leaving it at that for the moment)

Uncertain

If there is an industry that has no doubt on the reality of climate change, that’s the insurance industry. One of the key topic of the Geneva Association (one of the leading think tank of the insurance industry) is Extreme Event and Climate Risk. For a large part the insurance industry is relying on their historical data to derive their model around risk. However if conditions are changing rapidly, these models have a risk of becoming less relevant. This is forcing the insurance industry to reevaluate the way the work, for example fostering the creation of Open Source models and platforms. The OASIS loss modelling framework, fostered by Climate-KIC and the UK Knowledge Transfer Network, is an example of this type of approach. More generally, the emergence of cross industry data sources, models and the infrastructure to support it bear the promise to massively affect the way the brokerage and insurance industry is operating.

Finally, some of the early models of insurance were based on the sharing of risks and rewards by a community of people (in themutual insurance model, policy holders co-own their insurance company- Benjamin Franklin “launched” this model in the US). In the last years we have seen, via the Internet and mobile now that online communities have reached a scale of unheard scale. Combining the two to reinvent the mutual insurance is therefore bound to happen.

The early players in this field for example Friendsurance and Guevara, have both started from the brokerage spectrum of the industry (as it is a much easier entry point from a regulatory / capital point of view). My way of framing what they do is that it is a form of arbitrage on deductibles. By pooling an equivalent of a low deductible insurance subscription but effectively subscribing to a high deductible insurance product, they are creating a reserve pool of cash for the group to manage first claims. Pool creation and distribution of risk among pools, effective claim management, customer acquisition journey are the type of challenges these models are facing.

The emergence of blockchain / distributed application technologies has the potential to massively increase innovation in this space. A Blockchain based mutual insurance could not only distribute risks and ownership among members but also some of its infrastructure and logic including capital contribution. If you are thinking of doing something in that field, Eris Industries (disclosure: I am a non executive director and Anthemis is an investor) are the people you should talk to!

The Insurance Industry is about to change radically and rapidly, creating a massive opportunity for innovative companies to emerge and improve massively on the way insurance is built, bought and experienced.